Home / Business and Economy / Analysts Bullish on Tesla Despite EV Woes

Analysts Bullish on Tesla Despite EV Woes

8 Apr

Summary

- Tesla reported lower-than-expected Q1 2026 deliveries.

- Analysts maintain Buy ratings, citing future models and projects.

- New robot and truck production is slated for 2026 and 2027.

Tesla (TSLA) stock has experienced a year-to-date decline of 23% as of April 8, 2026, following lower-than-expected Q1 2026 deliveries. This downturn is attributed to concerns over electric vehicle sales amidst intense competition and economic uncertainty. Despite these headwinds, analysts from Canaccord and Cantor Fitzgerald have reiterated their Buy ratings for TSLA stock.

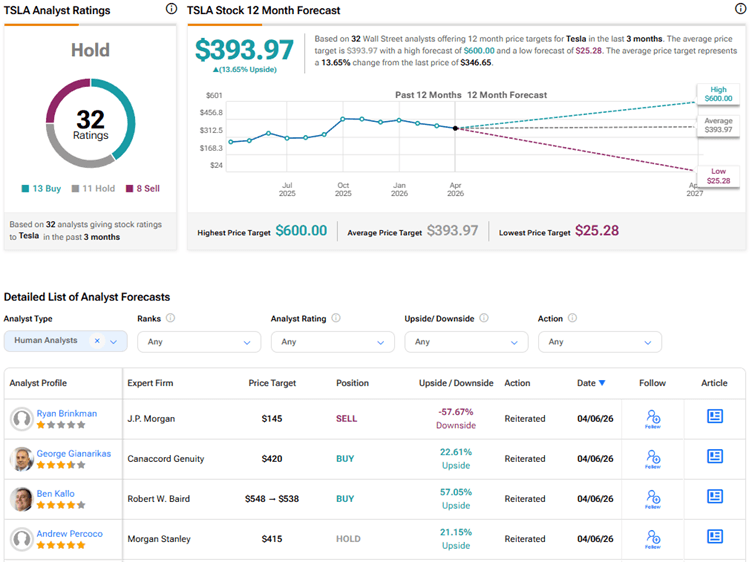

Canaccord analyst George Gianarikas maintained a Buy rating with a $420 price target, acknowledging the Q1 delivery miss but highlighting positive factors such as rising gas prices boosting EV interest and the potential of a new family-oriented Tesla model. Gianarikas also expressed optimism about Tesla's Terafab project for semiconductor manufacturing.

Cantor Fitzgerald's Andres Sheppard also reiterated a Buy rating, noting the missed Q1 energy storage shipments and a two-year decline in Tesla's vehicle deliveries. However, Sheppard remains bullish, citing the anticipated volume production of Cybercab, Tesla Semi, and Megapack 3 in 2026. Furthermore, initial deliveries of the Optimus humanoid robot are expected in the second half of 2027.

Wall Street's consensus rating for Tesla stock is currently Hold, with an average price target of $393.97, suggesting approximately 14% upside potential.