Home / Business and Economy / Bank of America Analyst Boosts AAPL Target

Bank of America Analyst Boosts AAPL Target

17 Apr

Summary

- AAPL bulls are optimistic ahead of Q2 FY26 earnings.

- Analyst Wamsi Mohan reiterated a Buy rating and raised AAPL price target.

- New AI-enhanced Siri and foldable iPhone are key future catalysts.

Apple's stock (AAPL) has seen a roughly 5% year-to-date decrease, attributed to concerns over input costs, tariffs, and uncertain consumer spending. However, ahead of its Q2 FY26 earnings report, optimism surrounds AAPL. Bulls point to a dedicated iPhone customer base and new products like the MacBook Neo.

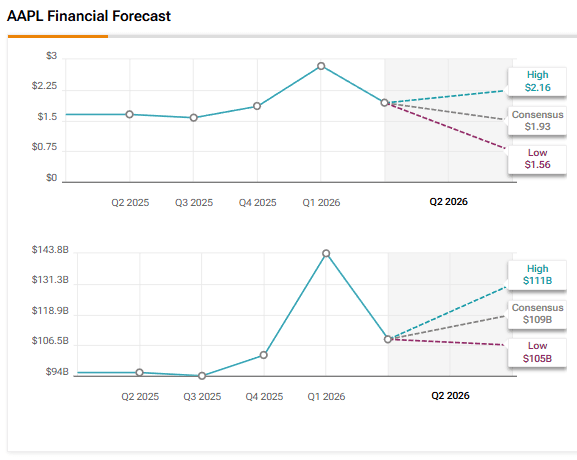

Top Bank of America analyst Wamsi Mohan has maintained a Buy rating on AAPL, increasing his price target to $325 from $320. Mohan expects Q2 FY26 results to exceed market expectations, driven by robust iPhone sales and growth in the Services division. Wall Street anticipates EPS of $1.93 and revenue of $108.86 billion for the quarter.

Mohan forecasts Q2 FY26 revenue, EPS, and gross margin of $113 billion, $2.00, and 48.2%, respectively, exceeding Street estimates due to strong iPhone sales, double-digit Services growth, and favorable currency exchange rates. Upcoming catalysts include a new buyback authorization, the WWDC event in June, and a potential foldable iPhone launch in the fall.

An anticipated Siri upgrade, integrated with Gemini AI, is also expected to drive further device upgrades. For Q2 FY26, Mohan raised his iPhone unit estimate to 60 million, projecting 14% year-over-year growth for Services revenue. He anticipates sequentially lower margins in Q3 FY26 due to product mix and component costs, forecasting Q3 revenue growth of 10%-15% and EPS of $1.82, also higher than Street estimates.

Currently, Wall Street maintains a Moderate Buy consensus on Apple stock, with 14 Buys, eight Holds, and one Sell. The average price target of $304.84 suggests approximately 18% upside potential.